The 4.35% Execution

Why the RBA is crushing the Australian mortgage belt to fight a Middle Eastern energy blockade.

Crushing the Australian Mortgage Belt

G’day.

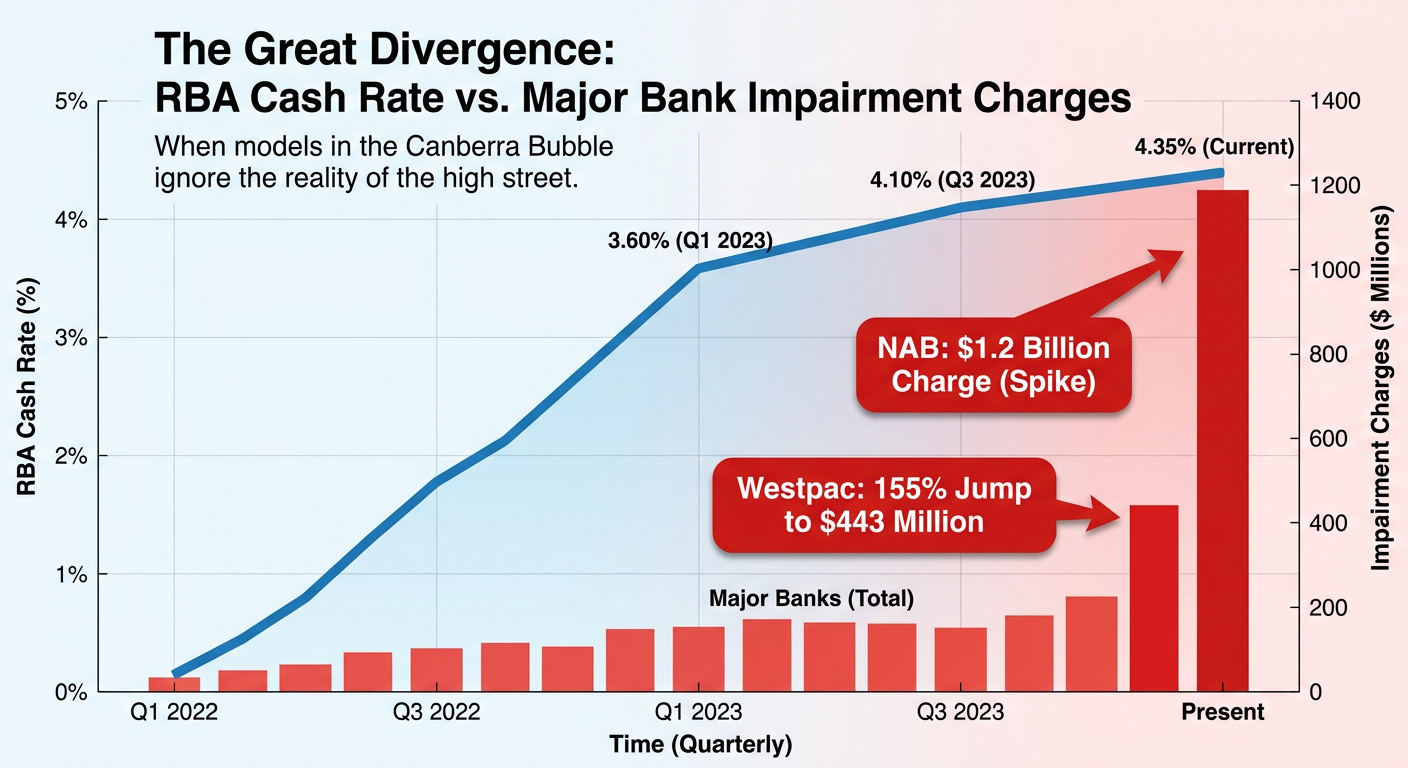

At 2:30 PM yesterday, the Reserve Bank of Australia officially chose to drop the hammer on the domestic private sector. By hiking the cash rate another 25 basis points to 4.35%, the RBA has deliberately tightened the screws on Australian families right in the middle of a synchronised global pause, record-low business confidence, and total chaos in the global energy supply chain.

To understand why this is happening, we have to look at the Axiom of Dual Coordination. Our economy is currently tearing itself apart as it tries to balance Ceremonial habits (the orthodox belief that central bankers must use interest rates to fight inflation, no matter what) against Instrumental reality (the actual physical supply of goods, fuel, and labour).

When the RBA released their official media statement yesterday, they proved just how trapped in the Ceremonial bubble they really are. Let’s disassemble the hallucinations they are trying to sell to the Australian public, starting with the banking sector’s latest “Revenue Mirage.”

1. The SME Slaughter (The NAB Autopsy)

The RBA claims: “Credit is readily available to both households and businesses.”

The Reality: This is a mathematically verifiable lie. Yesterday, we saw the National Australia Bank (NAB) post 8.7% revenue growth, but quietly swallow a catastrophic $1.2 Billion impairment charge.

NAB is Australia’s largest business bank. Their data is the definitive autopsy of the SME and Logistics sector. You cannot run a haulage company or a local tradie business without buying physical diesel today.

You cannot run a haulage company or a local tradie business without buying physical diesel today.

Small businesses are dying under the weight of the $3.29/L diesel shock and the RBA’s cash rate. NAB’s individual provision loss rates surged to an unprecedented 22 basis points—about six times the historical baseline.

Businesses aren’t gracefully transitioning; they are hitting the Solvency Wall at terminal velocity. Phase 1 of the pincer is executing right now.

2. The Hardship Mask (The Westpac Illusion)

Today, Westpac—the nation’s premier residential mortgage lender—dropped its half-year results. The establishment press is cheering because the CEO reckons “customers are resilient and stress levels have declined.”

That is an institutional hallucination. While an SME bleeds out immediately at the petrol pump, residential mortgages are shielded by the Hardship Mask.

Westpac has run off the cliff like Wile E. Coyote, but the statutory metrics haven’t looked down yet.

When a working-class family hits the wall, they drain their savings, max out the credit cards, and beg the bank for a 3-to-6-month “hardship variation” to pause repayments. This legally freezes the delinquency counter. Westpac claims stress has declined because their 90-day arrears metric fell slightly to 0.65%.

But look at the calendar: The reporting period ended March 31. A household completely crushed by the April 1 Toll Wall, the new diesel floors, and this latest 4.35% RBA detonation will not mathematically hit the 90-day arrears bucket until July. Westpac has run off the cliff like Wile E. Coyote, but the statutory metrics haven’t looked down yet.

The Smoking Gun: If Australian consumers are truly “resilient”, why is Westpac hoarding cash?

Their Total Impairment Charges just violently leapt 155% to a massive $443 million. Their internal models can see the furnace. They know the aggregate retail book is just masked by hardship variations, and they are hoarding capital because they know the household wall breaks in Q3.

3. The Baseline Hallucination

The RBA claims: “The baseline forecast, which assumes that the conflict is resolved soon and fuel prices decline...”

The Reality: This might be the most dangerous sentence in the RBA’s entire document. They are betting the mortgages of millions of Australians on the assumption that a massive geopolitical conflict in the Middle East will just politely wrap itself up, bringing the price of diesel back down.

No more TACO, now Trump’s a NACHO – find out why

They are entirely ignoring our Real Resource Vulnerability. As an island nation, we rely on imported refined fuels to run our transport networks and supply chains. The RBA has absolutely no model for a permanent biophysical supply shock. Instead, they just cross their fingers and hope the real world bends to their spreadsheets.

4. Administrative Violence Perfected

The RBA claims: “The conflict in the Middle East has resulted in sharply higher fuel... which are already adding to inflation. [...] It was therefore judged appropriate to increase the cash rate target.”

The Reality: Read that carefully. The central bank is explicitly admitting that inflation right now is being driven by foreign fuel shortages. And what is their chosen solution? To raise the mortgage payments and rent of Australian workers.

This is the terminal stage of Administrative Violence. They are attempting to cure a sovereign, supply-side physical shortage of energy by crushing domestic household demand. It’s like trying to fix a leaky pipe in your kitchen by setting your living room on fire.

The Verdict: The Q3 Panic Pivot

The pincer is closed. Phase 1 (The SME Slaughter) is already executing on the NAB ledger. Phase 2 (The Household Cliff) is ticking away quietly behind Westpac’s 90-day reporting lag.

The Godley Terminal is now officially locking its projection: When Westpac’s currently “resilient” households age out of their hardship pauses and transition into the 90+ days past-due bucket in July/August, the resulting avalanche of residential defaults will force the RBA into a panicked, emergency rate-cut cycle.

But as we have warned for months, this pivot will fail. Cheaper mortgages cannot refine diesel, clear the Strait of Hormuz, or plant winter wheat. We are on track for systemic fiscal intervention. The Scoreboard is about to catch up to the Structure.

The Lexicon (Updated)

Administrative Violence: The use of blunt technocratic tools (such as interest rate hikes) that knowingly inflict unemployment, poverty, or financial distress on the working class to protect Ceremonial economic targets.

The Hardship Mask: The temporary, 3-to-6 month mortgage repayment pauses banks grant to distressed households, which legally hides the true default rate from the statutory 90-day arrears reporting.

The Solvency Wall: The hard physical limit where a business or household entirely exhausts its cash buffers and credit lines, transitioning from “stressed” to bankrupt.

Real Resource Vulnerability: A nation’s physical dependence on essential imports (such as refined fuel), which cannot be solved by domestic financial manipulation.

The Baseline Hallucination: The orthodox habit of assuming complex, real-world physical or geopolitical crises will naturally resolve themselves to fit neatly back into a central bank’s inflation forecasting model.

The Lexicon (Updated)

Administrative Violence: The use of blunt technocratic tools (such as interest rate hikes) that knowingly inflict unemployment, poverty, or financial distress on the working class to protect Ceremonial economic targets.

The Hardship Mask: The temporary, 3-to-6 month mortgage repayment pauses banks grant to distressed households, which legally hides the true default rate from the statutory 90-day arrears reporting.

The Solvency Wall: The hard physical limit where a business or household entirely exhausts its cash buffers and credit lines, transitioning from “stressed” to bankrupt.

Real Resource Vulnerability: A nation’s physical dependence on essential imports (such as refined fuel), which cannot be solved by domestic financial manipulation.

The Baseline Hallucination: The orthodox habit of assuming complex, real-world physical or geopolitical crises will naturally resolve themselves to fit neatly back into a central bank’s inflation forecasting model.

From the Archives:

If you enjoyed this post, please consider buying me a coffee by pressing the button below.